Three years in: the maturation continues

As we enter 2026, we look at three full years of AI spending data across Australian SMBs.

This quarterly update covers Q4 2025 (October through December) plus January 2026, giving us our first complete three-year view of Australia's AI adoption journey at the ground level. And while the overall trend remains upward, the composition of that growth is starting to shift in ways that merit attention.

The headline story this quarter is Anthropic's growth, and it's relative acceleration versus OpenAI, likely propelled by the launch of Claude Cowork, the accleration of Claude Code after Christmas and industry-specific automation plug-ins in Jan of 2026. Our measures here coincides with global downgrade of SaaS and professional services public market valuations in early February as investors questioned whether AI agents could displace traditional software. Our data appears to capture this moment in real time, with Australian SMBs responding to Anthropic's aggressive B2B product push.

Snapshot of findings

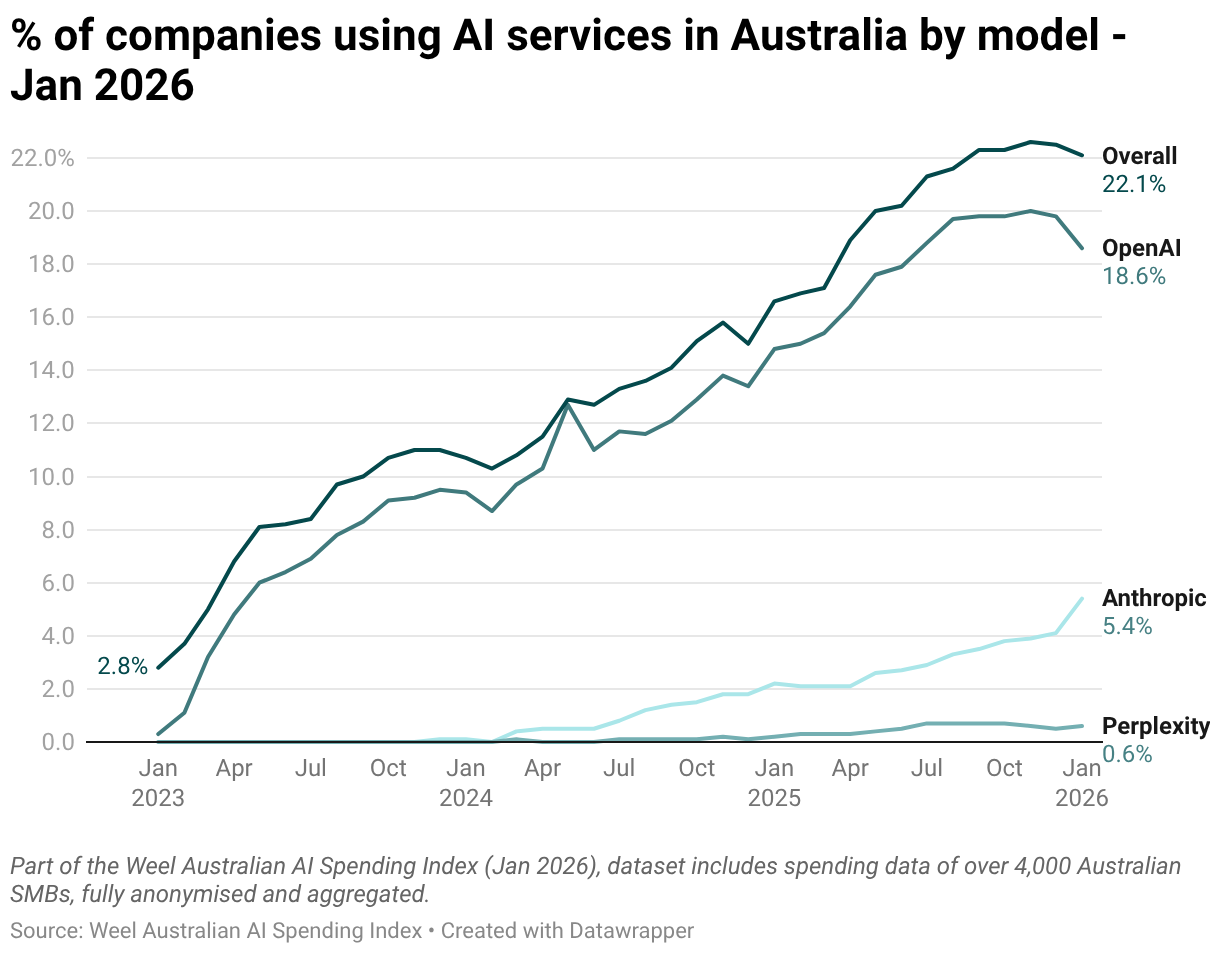

1. overall adoption nudges higher, with a seasonal january dip

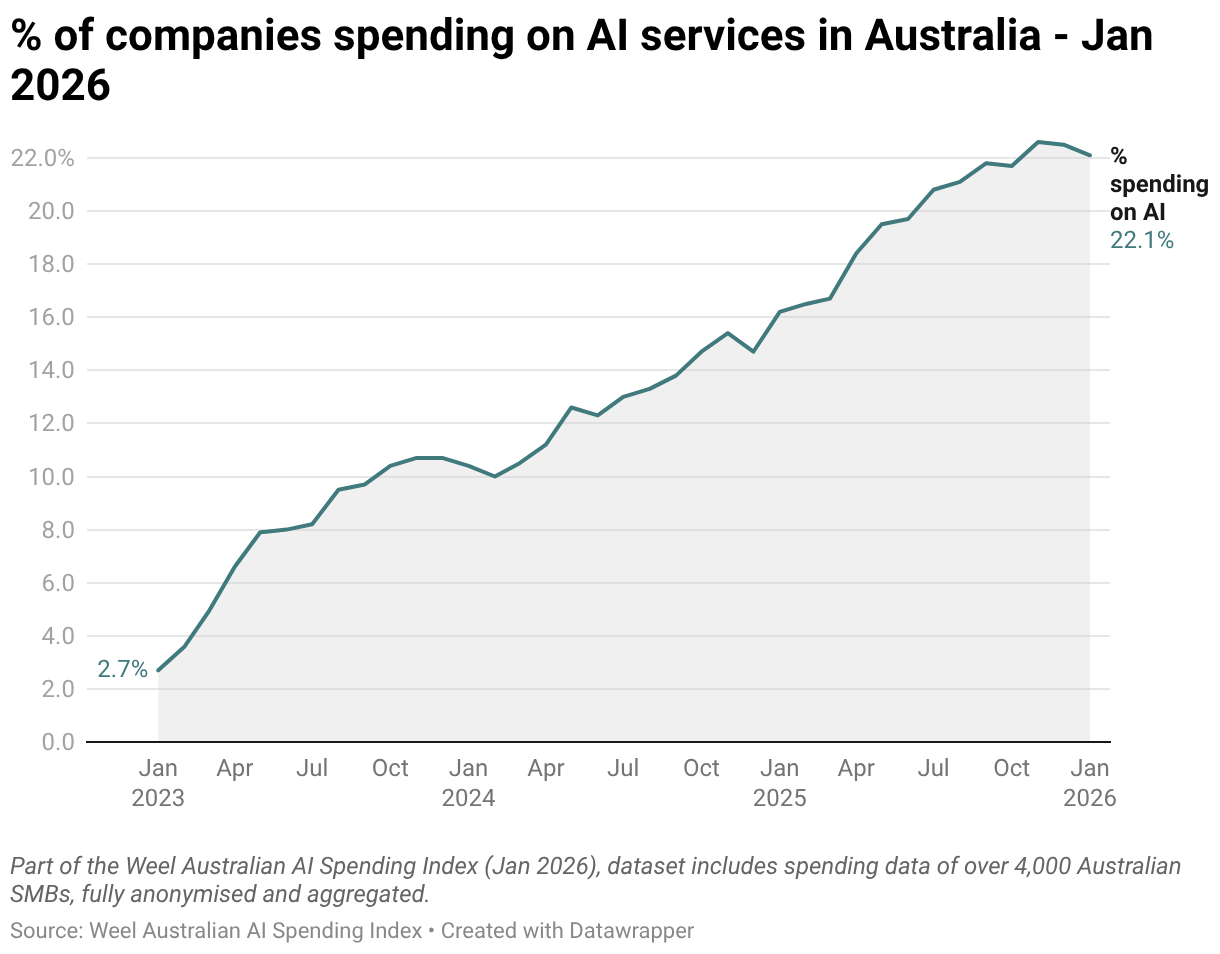

AI adoption among Australian SMBs reached 22.5% by December 2025, up from 21.75% in September. It's a modest quarterly gain, but the trajectory remains consistent with what we've observed throughout the year.

January 2026, however, saw a dip in overall spending - expected given the public holiday period and typical early-year budget resets. This seasonal pattern is worth noting as we continue to track quarter-over-quarter movements in a few months.

2. the Anthropic acceleration: a notable shift in service preference

The most significant development this quarter isn't in overall adoption - it's in the underlying trend between the two major AI platforms.

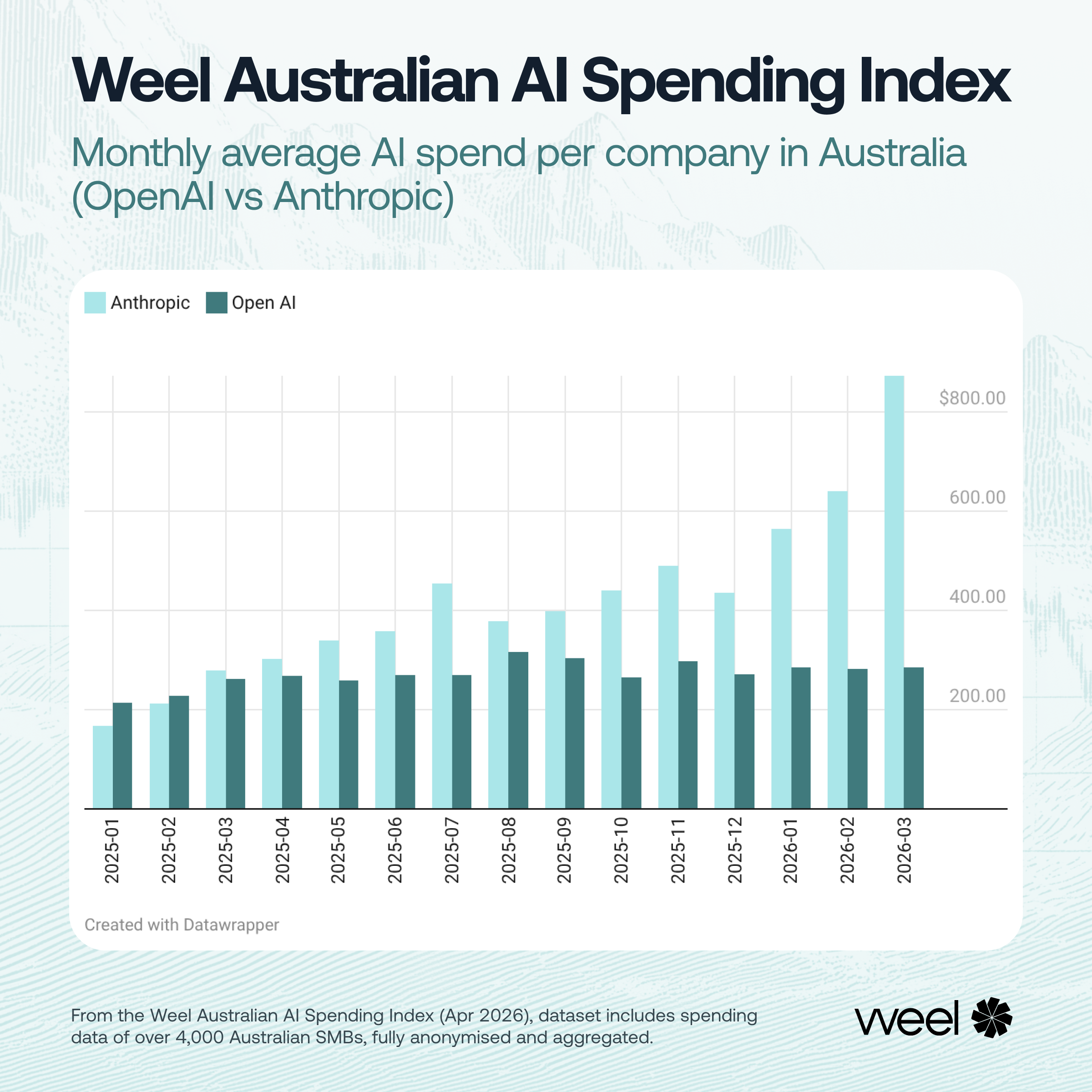

Anthropic is growing faster than OpenAI:

- Anthropic climbed from 3.5% in September to 4.1% in December, then surged to 5.4% in January 2026. That's an increase of 54% from September.

- OpenAI held relatively steady: 19.3% in September, 19.8% in December, then dropped to 18.6% in January. That's a drop of 6% from September.

This is the first time we've observed such pronounced divergence since January of 2024, when Anthropic first came onto the radar. While OpenAI still commands the lion's share of adoption, Anthropic's growth rate is worth watching.

The January decline for OpenAI could be seasonal noise - public holidays and budget resets affect all platforms. But it could also signal the beginning of genuine platform switching. We'll be watching the February and March data closely to determine whether this is a temporary blip or the start of a sustained rebalancing.

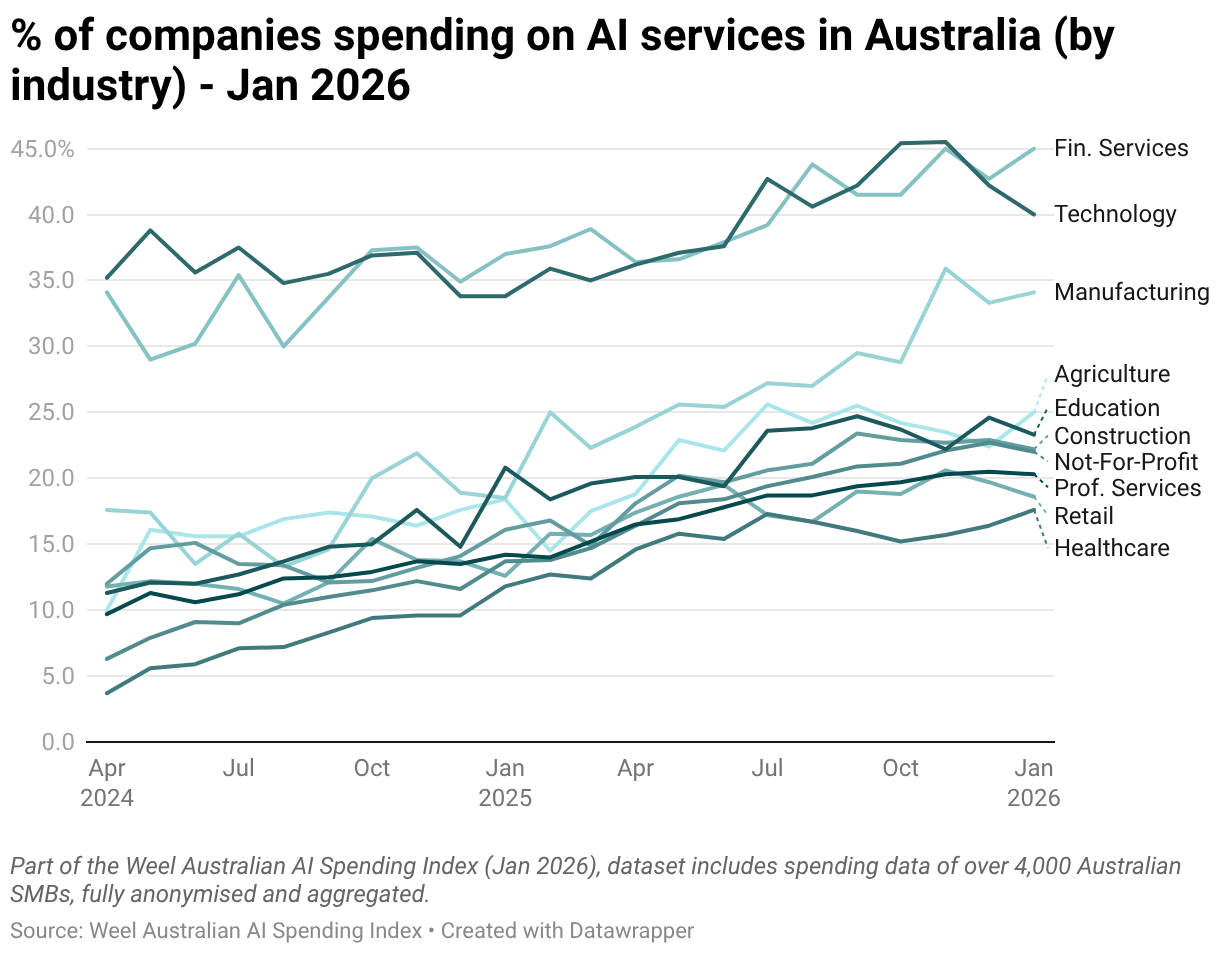

3. financial services overtakes technology as the AI adoption leader

This is presumably a reflection of LLM adoption increasingly becoming mainstream productivity improvement fare, as evidenced by product innovation like Cowork.

By January 2026:

- Financial Services: 45% of companies spending on AI

- Technology: 40% of companies spending on AI

- Manufacturing: 34.1% - now solidly in third place

This reversal is noteworthy. Technology companies have historically led adoption curves for emerging tools, but Financial Services has accelerated sharply over the past two quarters. The sector's regulatory complexity, documentation requirements, and operational scale may be driving a more aggressive push toward AI-enabled efficiency gains.

Technology's dip below Financial Services doesn't necessarily indicate a slowdown in absolute terms - tech remains well above the cross-industry average. But it does suggest that AI has become mission-critical in finance faster than in other sectors, where it may still be viewed as productivity-optional rather than competitiveness-essential.

Manufacturing, meanwhile, has consolidated its position as a strong third. At 34.1%, it's comfortably ahead of other sectors and showing steady quarter-over-quarter growth. The use case here appears operational: supply chain optimisation, quality control, and predictive maintenance rather than the knowledge-work automation driving adoption in Finance and Tech.

What we're watching

Platform dynamics

The Anthropic surge is the story of the quarter. Whether this represents temporary experimentation, genuine switching, or diversification into multi-AI stacks remains to be seen. January's sharp divergence could be an anomaly, but if February and March confirm the trend, it would mark a meaningful shift in platform preference among Australian SMBs.

Possible explanations include:

- Product improvements: Anthropic's recent model releases may have closed capability gaps

- Pricing pressure: Businesses exploring alternatives as OpenAI pricing matures

- Use-case fit: Anthropic's strengths in certain workflows (analysis, coding, reasoning) resonating more with SMB needs

- Diversification: Companies hedging against single-platform dependency

We'll need more quarters to determine causation, but the pattern is now clear enough to track deliberately.

Limitations (unchanged)

To maintain transparency, we reiterate the same limitations as our initial release:

- Company size representation: Data reflects Australian companies using Weel, biased toward SME adoption patterns

- Scope: This index is a leading indicator, not a comprehensive economic measurement

- Coverage window: Analysis now spans January 2023 - January 2026

- Exclusion of bundled AI services: Microsoft Co-Pilot and Google Gemini cannot currently be isolated from broader subscription SKUs

Stay updated

This index will continue to be updated quarterly as adoption accelerates and the dataset expands. The next scheduled coverage will be in Q2 2026.

For other deeper analyses and upcoming reports from the Weel Data Research series, please subscribe to our newsletter.