Expense management in Australia has a cost that most guides never mention: the cost of never being finished. The receipts sitting in a drawer for three weeks. The team member who has not submitted since February. The month-end that drags into the tenth because no one can account for the entertainment spend from last month's offsite.

This is not a process problem. It is a completion problem. And the difference matters, especially in 2026, when the Australian Taxation Office has moved from compliance education to active enforcement.

This guide covers what expense management is, what the ATO requires of your business, what the FBT shift of 2026 means for how you run your expense cycle, and what done actually looks like for finance teams in Australia and New Zealand.

What Is Expense Management?

Expense management is the system a business uses to capture, approve, code, and reconcile spending by its people. It covers the full cycle from the moment money leaves the business to the moment that transaction is verified, correctly coded for GST and FBT, and sitting clean in your accounting system. Expense tracking, expense reporting, and reimbursements are all components of this cycle — not separate processes, but stages within a single loop that either closes or it does not.

It is not the same as accounts payable. Accounts payable handles invoices from suppliers — money the business owes to external parties. Expense management handles spending that has already occurred, often initiated by individuals within your business, that needs to be captured, attributed, and closed.

The four components of every complete expense management cycle:

- Capture — Recording the spend. Receipt, card transaction, or mileage claim.

- Approval — Getting the right manager or finance contact to sign off.

- Coding — Applying the correct GST category, cost centre, FBT treatment, and accounting code.

- Close — The expense is reconciled, synced to your accounting platform, and no longer open.

Most Australian businesses have processes for the first two. The ones that run into trouble at FBT lodgement time are the ones that never close the loop on three and four.

An expense that is captured but not coded is not done. An expense that is approved but not reconciled is not done. Done means closed.

What the ATO Requires from Australian Businesses

The ATO does not care whether your expense management process is manual or automated. It cares whether your records are complete, accurate, and accessible.

Substantiation rules

Under the ATO's substantiation rules, businesses must retain written evidence for all work-related expense claims. For most expenses, that means a receipt, invoice, or document showing: the amount, the date, the supplier's name, and the nature of the expense. Credit card statements alone are not sufficient substantiation. You need the underlying documentation.

For travel and overtime meal expenses, diary evidence may also be required if the total exceeds certain thresholds.

Five-year record retention

The ATO requires businesses to retain records supporting income tax claims for five years from the date of lodgement of the relevant return. For FBT, records must be kept for five years from the date the FBT return was lodged or the date it was due, whichever is later.

That five-year window is not theoretical. The ATO's data matching programme cross-references third-party data from card providers, banks, and travel platforms against lodged returns. Incomplete records from three years ago become your problem in an audit today.

Digital receipts

The ATO accepts digital copies of receipts, including photos taken on a mobile phone, provided the image is a true and clear copy of the original. You do not need to keep the physical receipt once you have a readable digital copy.

This matters for your expense process. A receipt captured by OCR at point of spend, stored in your expense management system, and linked to the transaction record satisfies ATO substantiation requirements — provided the image is legible and the data is accurate.

GST and input tax credits

For GST-registered businesses, expense records must capture sufficient detail to support an input tax credit claim. That means: the supplier's ABN (or evidence they are GST-registered), the GST amount, the date of the tax invoice, and confirmation the expense serves a creditable purpose.

Many businesses lose GST input tax credits because their expense records do not capture the ABN or the GST line item. A receipt that reads "$110 — lunch" is not enough. A tax invoice showing "$100 + $10 GST, ABN 123 456 789" is.

For detail on ATO substantiation requirements, see ATO: Expenses you can claim.

FBT and Expense Management: What Changed in 2026

The FBT year closed on 31 March 2026. Paper returns are due 21 May 2026. Electronic lodgements via a registered tax agent are due 25 June 2026.

But the more significant shift is not the deadline. It is the ATO's posture.

ATO enforcement mode

The ATO has moved from an education-first approach to active enforcement. Enhanced data analytics and risk profiling now drive that enforcement. The ATO cross-references entertainment expense deductions against FBT returns, identifies businesses that claim entertainment deductions but lodge nil FBT returns, and targets vehicle benefit arrangements that misapply exemptions.

The five areas attracting the most ATO attention in 2026:

- Entertainment expenses. If you claim a deduction for meals or client entertainment, you should be accounting for FBT. If no FBT applies, no deduction should be claimed. The ATO identifies mismatches between income tax returns and FBT returns.

- Vehicle benefits. Businesses that provide vehicles for private use but fail to lodge an FBT return, and those that incorrectly apply the dual-cab ute exemption, are receiving increased scrutiny.

- Nil lodgements. Businesses that have historically not lodged FBT returns are being reviewed, even where they believe they have no FBT liability.

- Living-away-from-home allowances. The ATO is auditing whether LAFHA arrangements meet the conditions required for the available exemptions.

- Employee contributions. Reviews of whether contributions made to reduce FBT liability are being correctly documented.

What your expense management system needs to capture for FBT

For any expense that may attract FBT liability, your system needs to record:

- The type of benefit provided (meal entertainment, vehicle use, etc.)

- Who received the benefit (name and role)

- The business purpose and whether private use was involved

- The total value of the benefit

- For meal entertainment: the number of attendees and their employer or employee status

Without this data captured at the time of spend, you are reconstructing it at lodgement time. That is both time-consuming and audit-risky.

For the ATO's guidance on fringe benefits, see how fringe benefits tax works.

The Most Common Expense Management Failures in Australian Businesses

The following are not hypothetical scenarios. They are the patterns that show up repeatedly in mid-market businesses across Australia and New Zealand — and each one represents an open loop.

Late submissions that create FBT exposure

When team members submit expenses weeks after the spend occurred, the FBT year may have already closed. Entertainment expenses not captured in time cannot be retrospectively attributed to the correct FBT year. The result: either you lodge a nil FBT return that is technically incorrect, or you reconstruct records under time pressure with incomplete data.

The fix is not chasing people harder. It is removing the friction that causes late submission in the first place, and setting clear policy around entertainment categorisation at point of spend.

Manual GST coding errors

When expenses are coded manually, whether by your people or your finance team, GST is regularly miscoded. Meals become fully deductible. Entertainment with a business purpose gets mixed with entertainment that should attract FBT. The cost is not just the time spent correcting entries. It is GST input tax credits not claimed and FBT liability not accounted for.

No audit trail for entertainment

The ATO specifically looks for entertainment expense deductions not supported by FBT records. If your expense management process captures "client dinner — $420" without attendee names, an employer/employee split, and a business purpose note, you have no defensible audit trail.

Month-end drag from incomplete approvals

Finance closes when every expense is approved, coded, and reconciled. When approvals sit in inboxes or when team members have not submitted, month-end cannot close. The cost is not just the extra days. It is delayed management reporting, inaccurate cost centre visibility, and a finance team that is always catching up rather than closing.

Reimbursement delays that erode trust

When people pay out of pocket and wait two or three weeks to be reimbursed, they stop submitting promptly. The backlog builds. The expense management problem compounds.

Businesses using Weel see half of all reimbursements paid within 24 hours and 95% fully paid across the entire reimbursement cycle. That speed is not incidental. It is what prompt submission looks like when the friction is removed.

How Expense Management Works: The Full Cycle

A complete expense management cycle covers seven stages. The bottlenecks that cause month-end drag and FBT exposure almost always sit in stages three, four, and five.

Stage 1: Policy. Before any spend occurs, the business needs a clear expense policy: who is authorised to spend, on what categories, up to what amounts, and what pre-approval is required. Without this, every expense is a discretionary call — and discretionary calls create the gaps that auditors find.

Stage 2: Spend. The expense occurs. Card swipe, cash payment, or online purchase. If it is a corporate card transaction, the card system feeds the data. If it is a personal payment for later reimbursement, the clock starts on the submission process.

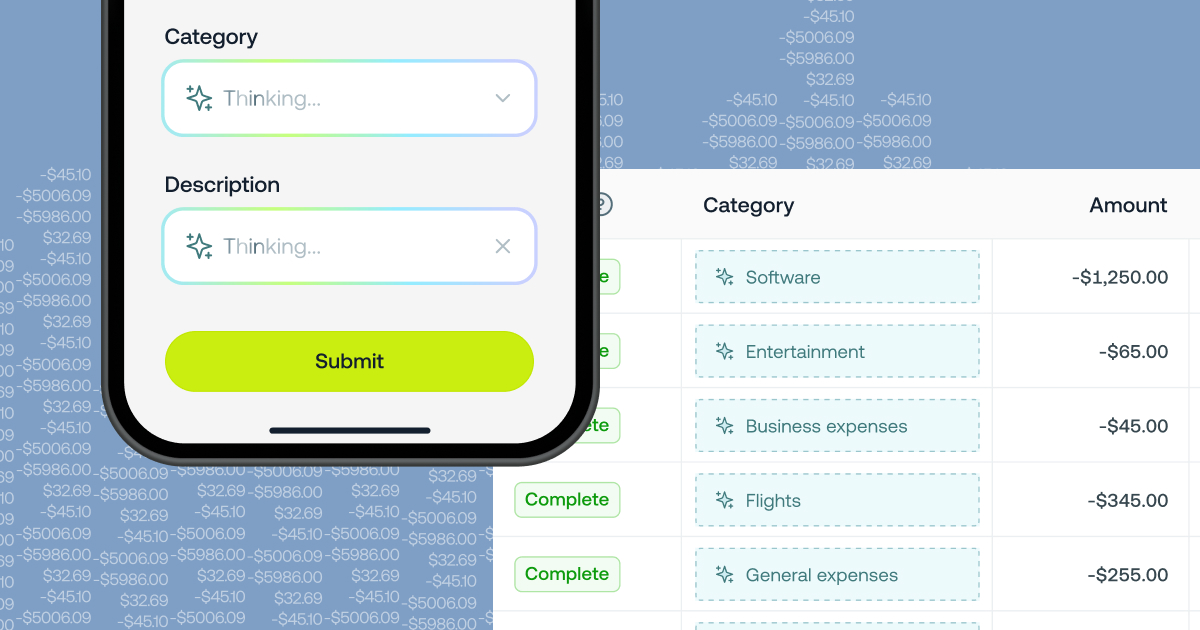

Stage 3: Receipt capture (OCR). The receipt needs to be captured at point of spend, not saved for later. Modern expense management systems use OCR to read the receipt immediately: amount, supplier, ABN, GST component, date. Captured at the moment of spend, the data is accurate. Captured three weeks later from a crumpled receipt, it is not.

Stage 4: Submission and approval. The expense is submitted through the system, routed to the appropriate approver based on policy, and approved or queried. Businesses using approval workflows reach 95% expense completion — approvals do not stall because they are automatically routed and tracked.

Stage 5: Coding (GST and FBT). The expense is coded for GST treatment and, where relevant, FBT categorisation. This is where most manual processes fail. Automated systems apply coding rules at submission — the expense arrives in your accounting platform already coded correctly.

Stage 6: Reconciliation. Card transactions are matched to receipts and expense records. Corporate card reconciliation confirms that every transaction on the card feed has a matching, approved expense record. Gaps in reconciliation are gaps in your audit trail.

Stage 7: Close. The expense is synced to Xero, MYOB, NetSuite, TechnologyOne, or your ERP. Coded. Reconciled. Closed. Not sitting in a draft. Not pending. Done.

When all seven stages run cleanly, expense management is not a month-end event. It is a continuous, real-time process — and the books are always close to closed.

Building an Expense Management Policy for an Australian Business

Your expense management system is only as complete as the policy it enforces. A policy that is vague, out of date, or not accessible to your people is not a policy. It is a document that no one applies.

A working expense management policy for an Australian business should cover the following.

Who can spend. Name the role types authorised to incur business expenses and those that require pre-approval for any amount. Be specific: a team member who travels regularly for client visits has different spending authority than someone who works from a fixed office location.

Spend categories and limits. Define the categories your business recognises — travel, accommodation, meals, client entertainment, office supplies, subscriptions, equipment — and set per-transaction and monthly limits for each. Entertainment limits should explicitly reference FBT: meals with clients above certain amounts trigger FBT obligations that the claimant needs to understand before they spend.

Pre-approval thresholds. Set the dollar threshold above which pre-approval is required before spend occurs. For high-value items such as flights, accommodation, and equipment, pre-approval prevents reconciliation surprises.

Entertainment rules. Entertainment is the highest-risk expense category from an FBT perspective. Your policy should require: attendee names, an employer/employee split, and a business purpose note for every entertainment expense. This data is what protects the business in an ATO audit.

Submission deadlines. Define how quickly expenses must be submitted after they are incurred. Weekly submission cycles are the minimum. Real-time submission at point of spend is the standard that modern expense management systems make practical.

Reimbursement timelines. State how quickly approved reimbursements will be processed. Vague commitments create the reimbursement backlog that drives late submission.

For ATO substantiation requirements your policy should reflect, see ATO: Expenses you can claim.

What to Look for in Expense Management Software in Australia

This is not a product comparison. It is a checklist for any finance manager evaluating expense management software for an Australian or New Zealand business. The items below are the ones that separate tools built for the local market from tools built for a generic global audience.

GST line-item extraction. The system must extract the GST component from receipt data, not just the total. Tax invoices show a base amount plus GST separately; the system must capture and code each field. Without this, your input tax credit claims require manual correction.

FBT categorisation. The system must support FBT categorisation at submission: meal entertainment, vehicle benefits, living-away-from-home allowances. If the system cannot distinguish a deductible client meal from an FBT-attracting staff entertainment event, the coding burden does not reduce. It shifts to your finance team.

Xero and MYOB integration. These are the two most common accounting platforms in the Australian mid-market. Your expense management system must integrate with both via a live feed, not a manual CSV export. For businesses on NetSuite or TechnologyOne, confirm the integration is certified and current.

Approval workflows. Look for configurable approval chains that route automatically by amount, category, cost centre, and role. Manual approval processes create the inbox delays that stall month-end close. Automated routing means approvals complete in hours, not days.

Corporate card reconciliation. If your business uses corporate cards, the system must reconcile card transactions against submitted expense records automatically. The reconciliation report should show, at any point in the month, which transactions are matched and which are outstanding.

Real-time spend visibility. Finance should see committed spend across the business in real time, not at month-end. Real-time visibility moves expense management from a periodic cleanup task to a continuous finance function.

Reimbursement speed. Ask vendors for their median reimbursement timeline. This is a real operational metric. When your people know reimbursements arrive the next day, they submit receipts at point of spend. When they wait three weeks, they do not.

Mobile receipt capture. Your people are not at their desks when they spend. The system must have a mobile app with OCR receipt capture that works offline and syncs when connected. Receipts captured at point of spend are accurate. Receipts submitted from memory a week later are not.

How Australian Finance Teams Use Weel for Expense Management

Weel is the expense management platform built for Australia and New Zealand businesses. It covers the full expense cycle — from card swipe to accounting sync — and closes every loop automatically.

When a business runs its expense cycle on Weel:

- Receipts are captured at point of spend via OCR on the mobile app, with ABN, GST, and supplier data extracted automatically.

- Transactions from Weel corporate cards feed into the system in real time and match to submitted receipts without manual reconciliation.

- Approval workflows route automatically by amount, category, and cost centre. No inbox management. No chasing.

- Reimbursements are processed in a single batch. Half of all reimbursements are paid within 24 hours. 95% are fully paid across the cycle.

- Every transaction syncs coded — GST, FBT category, cost centre, and accounting code — directly into Xero or MYOB.

Businesses using Weel's approval workflows reach 95% expense completion. Over 90% of card expenses reach full manager approval. The books are not waiting for month-end. They are always close to closed.

For businesses managing accounts payable alongside employee expenses, Weel covers the full spend picture — from individual card transactions to supplier invoices.

Expense management in Australia is complete when every receipt is captured, every transaction is coded, every approval is done, and nothing is sitting open. The FBT year has closed. The ATO is auditing. Month-end does not have to be an event. It can be already done.

Every Expense Complete.

See how Weel closes the expense loop for Australian and New Zealand businesses: take a product tour at letsweel.com.